Have questions about the new FHSA?

Published: Oct 17, 2022

Updated: Mar 19, 2026

Learn a few tips and guidelines to help you get the most out of your First Home Savings Account.

The First Home Savings Account is a great investment tool that is designed to empower Canadians to become homeowners. However, not everyone’s situation is the same, and you may find yourself running into some gray areas with how to handle your FHSA.

We’ve got you covered.

What counts as a ‘home’ for FHSAs?

The definition of a ‘home’ is important with FHSAs: you cannot open an FHSA or make a tax-free withdrawal if you or your spouse have lived in a home you’ve owned this year or in any of the last 4 calendar years, and you can only make tax-free withdrawals if purchasing a qualifying home.

Please note that, while the government has not provided specific guidance for FHSAs, we can find answers to these questions by looking at the definitions used for the Home Buyer’s Plan.

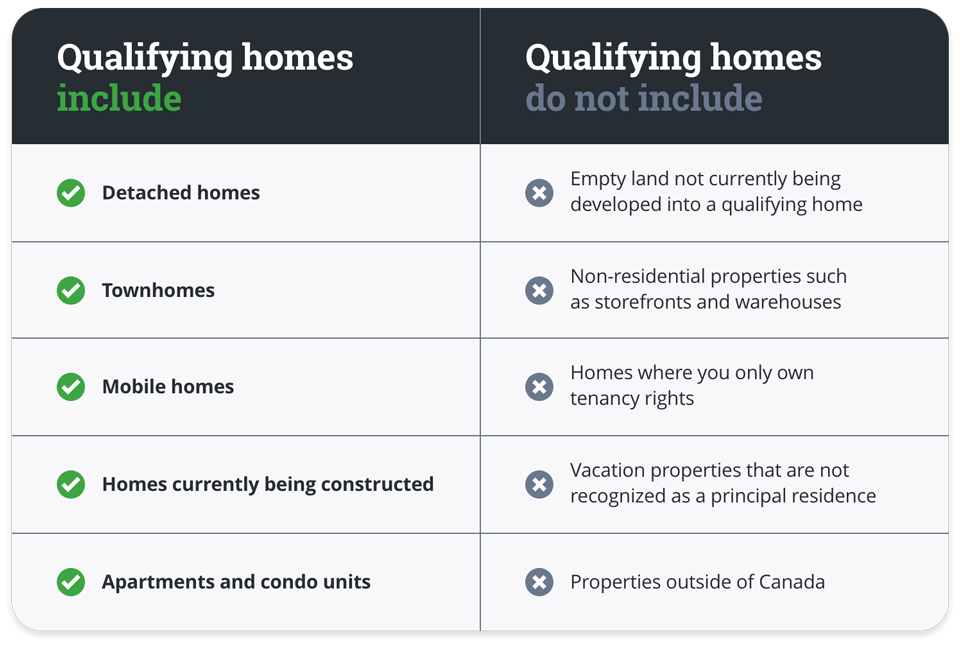

Does land without a house, an apartment/condo unit, a mobile home, or a summer home count as a home?

It depends on the nature of the property. Here are some common examples:

Does partial ownership of a home count?

Co-operative ownership of a home may count as homeownership, depending on the percentage of your stake.

Ownership of less than 10% doesn’t qualify as homeownership of a qualifying property. This means you can use your FHSA to purchase a stake of more than 10% in a qualifying property, but will be unable to open an FHSA if you have over 10% ownership of your current home.

Can I open an FHSA if I own property I don’t live in, like a business or rental property?

According to the government’s definition of homeownership as outlined in the RRSP Home Buyer’s Plan restrictions, any home that you do not live in, or do not intend to live in if the unit is under construction, does not count against your status as a first-time homeowner. Unless otherwise specified in further legislation, these same definitions should apply to FHSA qualification.

Other qualifying conditions

Many of the conditions surrounding the FHSA have to do with what counts as a ‘qualifying home’, but not all of them. These questions may also have an impact on your eligibility.

Can I open an FHSA if my spouse or common-law partner owns our home?

No. In the case of a legally recognized union or common-law status, homeownership applies to both partners regardless of whose name is on the deed. However, if you do have an FHSA when you get married or become common-law, you will still be allowed to contribute to it if you wish, and its deadlines will remain the same.

Can I open an FHSA if I previously owned a home?

As long as you haven’t lived in a qualifying home owned by either yourself or your spouse or common-law partner either this year or in the previous 4 calendar years, then you will be able to open and use a new FHSA.

What happens if I move outside of the country?

You must be a Canadian resident for tax purposes to open an FHSA, but if you already have an existing FHSA then you will be able to continue to contribute as a non-resident taxpayer (opens in a new tab). Your contribution limits will continue to grow and the required closing dates will still apply, however you must be a Canadian resident (opens in a new tab) to make a qualifying withdrawal.

Withdrawing or moving funds from your FHSA

Learn what happens when you move your money, whether you’re withdrawing to purchase a home or transferring to a different account.

Can I still make a Home Buyer’s Plan (HBP) withdrawal from an RRSP if I use an FHSA?

Yes. While the early version of the legislation that introduces the FHSA said that you were limited to using one or the other, the final version of the legislation allows you to withdraw tax-free funds from your FHSA and still qualify for an HBP withdrawal from your RRSP.

Can I only use the funds for the down payment?

There are many expenses associated with buying a new home, such as closing costs, legal fees, and moving costs. If available, you can withdraw as much as you want to cover these extra fees or any associated expenses beyond your down payment.

What happens to the account after 15 years, or after my 71st birth-year?

A notice will be issued before the account needs to be closed, at which point it can be transferred to an RRSP or RRIF with no tax penalties, or withdrawn as taxable income and subjected to withholding tax.

Will I be charged a de-registration fee when I close my FHSA?

No. Questrade currently does not charge a de-registration fee when you close an FHSA, regardless of whether or not you have made a qualifying withdrawal.

Can I use my FHSA to contribute to another registered account like a TFSA or an RRSP?

It is possible to transfer your FHSA to any registered account that allows contributions, but only transfers to RRSPs, RRIFs, or other FHSAs can be sent without tax penalty or changes to your contribution rooms. Transfers to other account types will be treated as withdrawals from the FHSA, treated as taxable income, and subject to withholding tax.

Do withdrawals reinstate contribution limits like in TFSAs?

No. Unlike TFSAs, which add withdrawn amounts to your next year’s contribution room, the FHSA does not reinstate contribution limits after withdrawal for any reason.

What is the minimum amount of time funds must be in an FHSA before making a qualified withdrawal?

Questrade FHSAs have no minimum period before you can make a qualifying withdrawal. If you find the home that’s right for you earlier than you expected, you don’t have to worry about your funds being tied up to meet some minimum time requirement.

It’s worth mentioning that the earlier you open an FHSA account the more time you have to build your contribution room, and the more time for tax-free growth you give the money you contribute.

How long will it take to process a qualifying withdrawal from an FHSA?

We are currently handling qualifying withdrawals using the same timelines as we apply to the Home Buyer’s Plan, which typically involves a review period of up to 5-10 business days to make sure the documents are all in order.

Please keep in mind that timely processing requires accurate information on the forms. Inaccurate information will lead to additional time delays.

If your request is rejected due to discrepancies in your forms, you will be notified via email with further instruction.

What happens if I have money left over after buying a property?

You have until 30 days after you move into your home to withdraw funds tax-free to put towards expenses. After this grace period, you have until December 31st of the following year to transfer any remaining funds to an RRSP or RRIF with no tax penalties, or withdraw remaining funds as taxable income subject to withholding tax.

Can I make a tax-free withdrawal from an FHSA to buy property outside of Canada?

No. Homes must be within Canada to qualify for tax-free withdrawal.

What happens if I make a non-qualifying withdrawal?

If you make a withdrawal that doesn’t qualify as tax-free, the funds you withdraw will count as taxable income and be automatically subject to withholding tax.

Since the government has not provided specific guidance for how this is to be taxed for FHSA withdrawals, the non-qualifying withdrawal will be taxed at the current RRSP withholding tax rates until otherwise instructed.

To learn more about taxable income and withholding tax, please contact your accountant or tax advisor.

Do qualifying FHSA withdrawals have tax implications in other countries?

While qualifying withdrawals from an FHSA are not taxed by the Canada Revenue Agency, they may have tax implications from other governments. If you might be subject to tax in a jurisdiction outside of Canada, please contact an accountant or tax advisor.

Contributing to your FHSA

Learn the benefits and limitations of using different methods to contribute to an FHSA account.

What is my deadline to contribute to count as a contribution for this calendar year?

The FHSA deadline is December 31, but depending on how you fund your account there might be some time required for the funds to deposit into your account.

The fastest method of funding is Instant deposit. For a full description of the funding methods available at Questrade (and how long each of them can take), please refer to our article on funding your account.

When do contributions to an FHSA qualify for tax benefits?

The timing of your FHSA contribution will affect which year it’s applied to. This depends on the deposit method you used and when you started the deposit. We encourage you to make your contribution well before the end of the year however if you wait until the last minute here's how your contribution may be treated:

Instant deposit: Instant deposits received by Questrade prior to midnight on the last business day of the year will be considered a contribution for that year.

Online bill payment: Online bill payments initiated in the previous year but received on the first business day of the new year will be considered a contribution for the previous year.

Online bill payments (delayed): Online bill payments received on or after the second business day of the new year will be considered a contribution for the current year. If you initiated the payment in the previous year and intended it to be a previous year contribution, please contact client services to backdate your contribution. You will need to provide us proof of deposit payment initiation date.

Can I use my TFSA to contribute to my FHSA?

Yes, you can! Money transferred from your TFSA is treated as though you had withdrawn the funds and then deposited it to your FHSA: the FHSA contribution can be claimed as a deduction on your Canadian tax return, and you will regain the TFSA contribution room the following year.

Note that if you are subject to tax in a jurisdiction outside of Canada, there may be tax implications from other governments. Please contact an accountant or tax advisor if this applies to you.

Can I use my RRSP to contribute to my FHSA?

Yes, you can… but keep in mind that money transferred from your RRSP cannot be claimed on your taxes (as the underlying funds have already been claimed as RRSP contributions), will not return your RRSP contribution room, and will count against the available contribution room in your FHSA.

Can I open a joint account with my significant other?

While you cannot open a joint account, you can both open and use your separate FHSAs for your first home. This means that you will not be able to contribute directly to your partner’s FHSA as you would into a joint RRSP; your partner will need to make any contributions into their own FHSA account.

What happens if I open an account before the end of the year and don’t fund it?

Your contribution room begins to accumulate from when your account is opened, so if you open your account in December of one year, that contribution room carries forward into that next year.

Do I need to claim my FHSA contributions right away?

No. Like RRSP contributions, FHSA contribution claims can be delayed at your discretion. This may be handy if you intend to plan your FHSA claims around your tax schedule. To learn more, please contact your tax advisor.

Can I participate in active trading in my FHSA account?

While Questrade does not place any trade volume restrictions on any registered accounts, the CRA may classify gains that result from active trading in tax-free registered accounts as taxable business income. If you plan on participating in high-volume trading, contact your tax advisor.

Are U.S. dividends subject to withholding tax?

U.S. dividends earned in an FHSA are subject to U.S. withholding tax.

In this context, withholding tax is a tax placed on dividends from U.S. securities paid to Canadian investors. While RRSPs aren’t subject to such taxes, TFSAs and FHSAs have a 15% withholding tax on U.S. company dividends, as required by the IRS.

Is there a minimum amount I need to contribute to an FHSA?

While there is no minimum amount you are required to open an FHSA account, the minimum balance requirements for investing in Questrade accounts still apply.

You will be able to open an FHSA account with a lower balance, but you will not be able to invest until the minimums are met.

The FHSA as an asset

FHSAs are handled differently from other registered accounts in several ways.

How are FHSAs handled in a divorce?

FHSAs are counted the same as any other asset in a divorce.

As a part of a settlement, an FHSA can be transferred to the other party’s FHSA, RRSP, or RRIF without incurring any tax penalties. In this case, it would not use the contribution room of the recipient, nor restore any contribution room from the transferrer.

Recipients would still be subject to FHSA restrictions, such as the age limits and homeownership status. If the recipient is ineligible to open an FHSA, the balance can be transferred to an RRSP or RRIF instead without incurring tax penalties.

What happens if an FHSA is inherited?

The account holder of an FHSA will be able to designate beneficiaries as they would with any other registered account. If the FHSA is inherited by a current spouse, then it can be transferred into an FHSA or RRSP without tax penalty. Otherwise, it will be subject to withholding tax before ownership is transferred.