Guaranteed Investment Certificate (GIC)

Published: Oct 17, 2022

Updated: Apr 10, 2026

Buy GICs online with Questrade to help diversify your portfolio and provide steady fixed-income.

A Guaranteed Investment Certificate (GIC) is a secure investment product that can offer a fixed rate of return on your deposited funds for a specific time frame.

When you purchase a GIC, you're lending your money to banks, trust companies, or other financial institutions for a specific length of time. In exchange, you're guaranteed a set interest rate on your investment.

GICs are similar to bonds in that they both provide a fixed return and are considered lower-risk investments. Learn more about fixed-income trading for bonds and GICs here.

Every GIC available through Questrade is issued by either a CDIC member organization (opens in a new tab), or an FRSA regulated Ontario credit union (opens in a new tab), so you can rest assured that your money’s protected¹ while it earns you interest.

Benefits of GICs

Stability in high-interest-rate environments: GICs can be particularly beneficial during times of high interest rates, as they provide a guaranteed return on investment that is unaffected by market fluctuations.

Portfolio diversification: Including GICs in your investment portfolio can help diversify your holdings, reducing overall risk and providing a more stable income stream.

Capital preservation: As GICs offer a guaranteed return, they're an excellent choice for conservative investors looking to preserve their capital while earning a modest return.

Get a Competitive GIC Rate Today

From 30 day terms up to 5 years, GICs are available for every type of investor.

If you don’t have a Questrade account yet, you can conveniently browse the most up-to-date GIC rates available with the link to our Bond bulletin. The Bond bulletin shows 30-270 day GICs on the first page, 1-5 year GICs on the second page, and a list of municipal and corporate bonds after that.

This PDF document is updated daily Monday through Friday shortly before the market opens at 9:30am ET.

Note: If the page does not refresh after the daily update, please try clearing your browser cache/cookies then reloading the Bond bulletin.

Buying GICs with Questrade online

Questrade offers an easy way for both new and experienced investors to invest in and explore various GICs online. With just a few clicks, you can effortlessly research and make purchases.

Trading GICs with Questrade is commission free², and you’re able to browse the most competitive rates available to pick the one most suited for your personal goals and needs.

Note: Most GICs are a minimum order of $5,000. Certain GICs may have higher minimums.

Take advantage of Questrade's user-friendly experience as you work towards growing your investment portfolio and building your wealth.

There are multiple ways to buy bonds and GICs through the trading platforms:

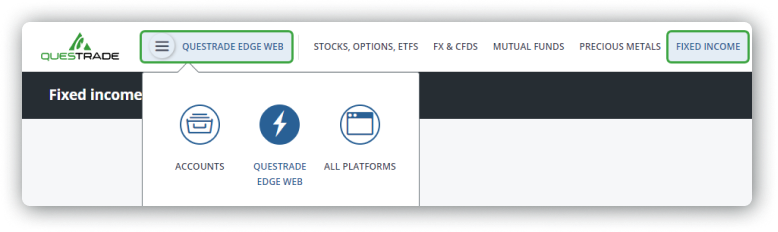

If you have Questrade Edge Web added:

On the top navigation bar, head over to the Fixed Income page under Accounts > Questrade Edge.

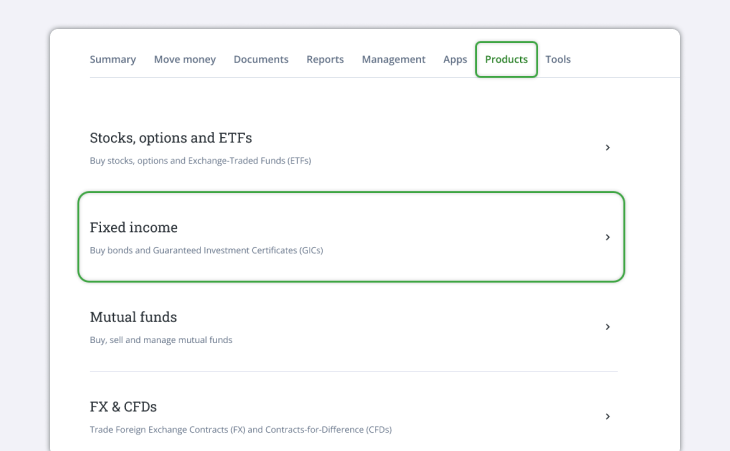

If you don't have Edge Web enabled:

Head over to the Products tab on the top navigation bar and select the Fixed income option.

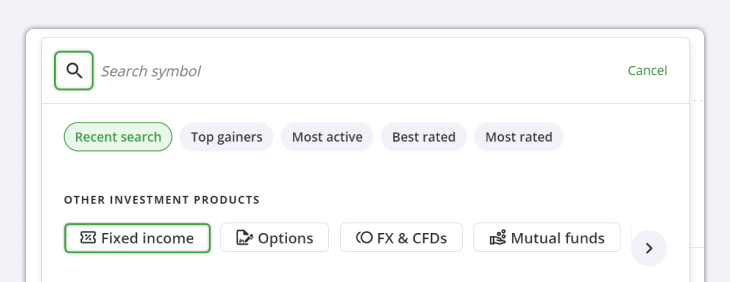

You can also access fixed income products through the search bar on the Summary page. You can either look up a specific bond or GIC directly, or you can select the Fixed income option from the drop-down menu in the symbol search.

GICs can be purchased through the fixed income platforms from 9am - 1pm ET. (Excluding weekends/holidays)

Ready to dive deeper into trading GICs online? Explore our lesson on fixed income trading.

There are two types of traditional GICs:

Cashable/Redeemable GICs: These GICs allow for early withdrawal of funds before the maturity date without incurring any penalties.

Non-cashable/redeemable GICs: With these GICs, your funds are locked in for the entire term, and the issuer doesn't permit withdrawals before the maturity date.

Generally, non-cashable GICs offer higher interest rates compared to cashable GICs.

If you choose to redeem a cashable GIC early, you must wait until after the redeemable term has passed. This is usually between 30 and 90 days after your initial purchase date. After redemption, interest will be calculated based on the total amount of days the GIC was held.

Example: Joanna buys a 1-year cashable GIC with a rate of 4.35%, and a redeemable term of 90 days for a total of $10,000. She’s planning on locking in her money for a year, but likes the option to access it after 3 months in case of an emergency.

After 6 months, some unexpected expenses arise, and Joanna decides to redeem her GIC early. Interest is calculated based on 6 months (180 days) at 4.35% yearly (not compounded), and gives her $214.52 which is added to her principal amount of $10,000 and paid to the account the GIC was purchased in.

Compound and Payment Frequency

Understanding the compound and payment frequency of GICs is crucial for investors to maximize their earnings and align them with their financial goals. At Questrade, GICs come with varying compound and payment frequencies, tailored to different investment strategies.

Annual Compounding

Annual compounding in GICs refers to the process where the interest earned on your initial investment (principal amount) is reinvested each year. This means that each year, you earn interest not only on your initial investment but also on the interest accumulated from previous years. You earn interest on your interest!

It's a powerful tool for long-term growth, as it allows your investment to grow at an accelerated rate over time.

For instance, if you invest in a GIC with a yearly compound interest rate, the interest is calculated and added to your principal at the end of each year. This compounded amount then serves as the new principal for the following year's interest calculation. This cycle continues until the GIC matures.

Example: Ted invests $20,000 in a 3-year non-cashable GIC with a rate of 4.2% that compounds annually. After the first year, he earns $840 in interest, then for year 2 he’s now earning 4.2% on $20,840. At the end of year 2, he earns $875.28 in interest, and for his third and final year, he’s now earning 4.2% on his total principal amount of $21,715.28. At the end of his final year he’ll receive another $912.04 in interest, and the total paid back to his account at maturity is $22,627.32 for a total gain of $2,627.32 after three years.

Compared to a GIC that pays out interest every year and does not compound, Ted has earned an additional $107.32. With larger or longer-term investments, this can make a big difference in the total amount you earn from a GIC.

Learn more about the magic of compound interest here, and how it can help accelerate your wealth accumulation.

Payment Frequencies: Annual or at Maturity?

GICs through Questrade offer different payment frequencies: annual payments or payments at the end of the GIC term. The choice between these options depends on your need for regular income versus maximizing growth potential.

Annual Payment Frequency: In this arrangement, the interest earned on your GIC is paid out annually. This is a popular choice for investors who desire a steady stream of income from their investments.

For example: A $100,000 GIC with a 4.5% annual interest rate will yield $4,500 each year. This option is ideal for those who need periodic payouts, such as retirees looking for a consistent income source.

Payment at Maturity: Alternatively, some investors prefer to receive their interest payments at the end of the GIC term. This option allows the interest to compound annually and be paid out in a lump sum when the GIC matures.

It's an excellent choice for those who do not need immediate income and want to maximize their investment growth. For example, a $10,000 GIC with a 4.5% interest rate compounded annually over a 5-year term will yield $2,462!

This significant lump sum at the end of the period reflects the total principal plus compounded interest.

Choosing between annual payments and payments at maturity depends on your financial objectives. If regular income is a priority, annual payments might suit you better. However, if your goal is to maximize growth, waiting for a lump sum at maturity is likely the more beneficial approach.

Whatever your goals, we’re here to help. Questrade offers GICs with flexible compound and payment options to fit various investment strategies and needs.

Important to know

GICs can be purchased in registered accounts including the TFSA, FHSA, RESP and more.

Generally, GIC interest is not taxable in registered accounts.

GICs are also available in non-registered Margin accounts

Non-cashable/redeemable GICs lock in your funds until the maturity date.

Consider GICs with different maturity dates to ensure you have access to funds when needed and to reduce the impact of interest rate fluctuations on your investments.

Depending on the GIC, interest payments may be paid to investors annually, or only upon maturity.

Interest is paid to the same account the GIC was originally purchased in.

GIC interest may be considered taxable income if the GIC is purchased in a non-registered Cash or Margin account. Yearly slips like the T5, RL-3, or NR4 will be generated for you during tax season.

Contact the Trade Desk to redeem a cashable/redeemable GIC.

At 1-866-980-9590 Monday to Friday, 7 am to 8 pm ET.

There are no fees charged to redeem a cashable GIC through the trade desk.

It may take some time for Questrade to receive your funds from the GIC issuer. Please allow 3-5 business days for accrued interest to appear in your account.

For a non-cashable/redeemable GIC, your funds (principal and interest) are automatically received in your account 3-5 business days after maturity.

You do not need to take any action prior to this date.

Keep more of Your Money

Ready to invest? Open a Questrade account and experience seamless, secure investing today.