The key to your first home

Power up your down payment with the tools and features to maximize your tax-free growth.

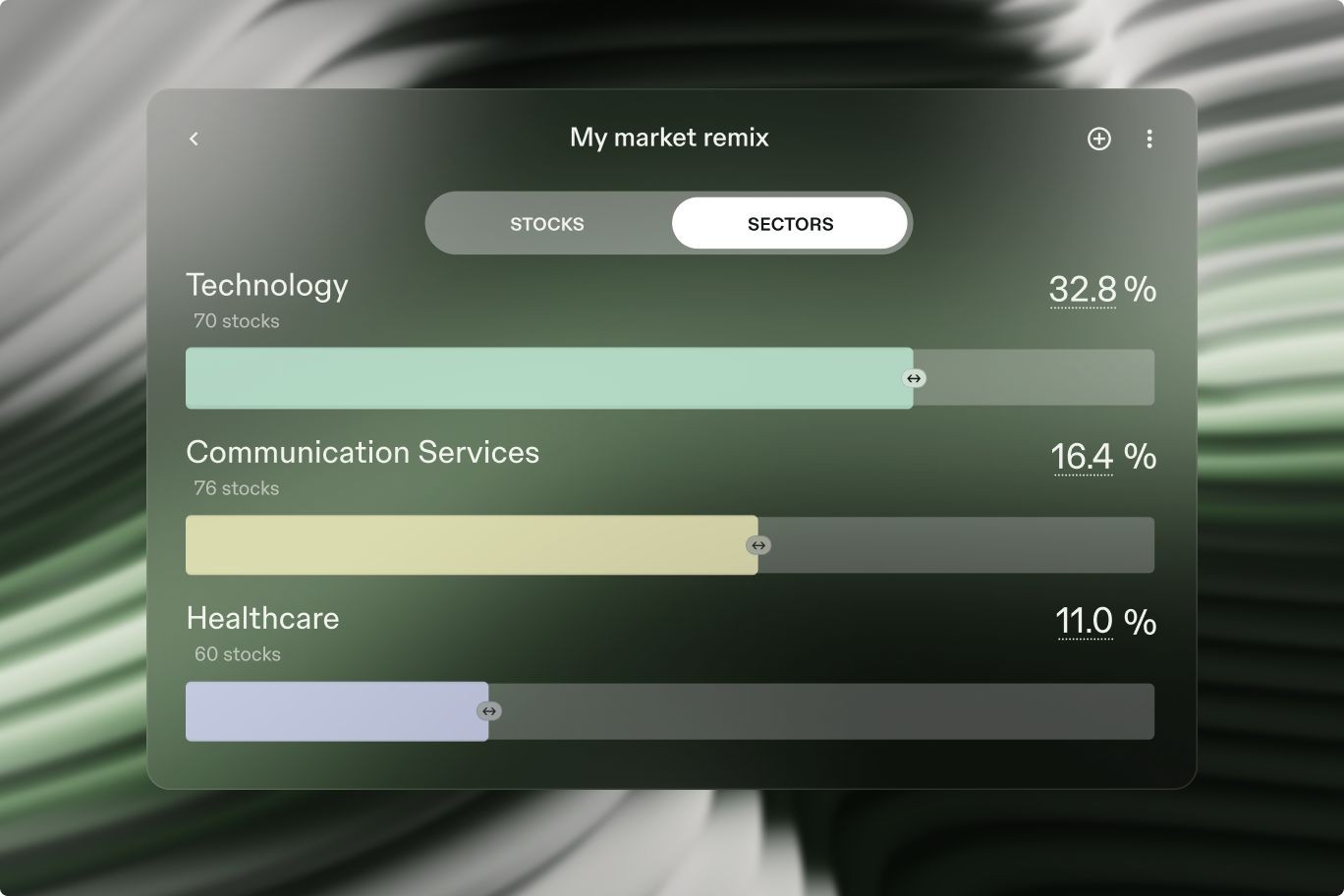

Two tax benefits, one account. Build your down payment faster with the First Home Savings Account.

Lower your tax bill

with all contributions up to your annual max

100% tax-free returns

when put towards a qualifying first home

Contribute up to $8,000

every year, up to $40,000 total

15 years to save

after that, your FHSA rolls over into an RRSP

Power up your down payment with the tools and features to maximize your tax-free growth.

Every dollar you contribute to your FHSA goes towards reducing your taxable income, while every withdrawal for an eligible home purchase is tax-free.

Invest, track, and manage your FHSA as part of your full financial portfolio. If you don’t end up buying a home, you can transfer the funds to your RRSP.

Contribute up to $8,000 per year, and $40,000 overall. Withdrawals can be combined with the RRSP Home Buyers’ Plan to unlock an extra $60,000.

The Globe and Mail“Some brokerages have low fees, others have good service, others have excellent platforms and a variety of investment products. Questrade has it all.”

Invest in your future with tax savings today. Every dollar you deposit in an RRSP lowers your taxable income and grows tax-free until it’s withdrawn.

Save for any goal, big or small, with the most flexible registered account. In a TFSA, your investments grow tax-free and can be withdrawn anytime for any reason.

Set your kids up to go as far as their dreams take them. With an RESP, contributions are matched by the government and grow tax-free.

Invest without any ceiling. No contribution limits, no withdrawal rules, no deadlines.

Access additional buying power and trade beyond your balance on margin, giving you the flexibility to act on opportunity.

Invest in your future with tax savings today. Every dollar you deposit in an RRSP lowers your taxable income and grows tax-free until it’s withdrawn.

Save for any goal, big or small, with the most flexible registered account. In a TFSA, your investments grow tax-free and can be withdrawn anytime for any reason.

Set your kids up to go as far as their dreams take them. With an RESP, contributions are matched by the government and grow tax-free.

Invest without any ceiling. No contribution limits, no withdrawal rules, no deadlines.

Access additional buying power and trade beyond your balance on margin, giving you the flexibility to act on opportunity.

Invest in your future with tax savings today. Every dollar you deposit in an RRSP lowers your taxable income and grows tax-free until it’s withdrawn.

Save for any goal, big or small, with the most flexible registered account. In a TFSA, your investments grow tax-free and can be withdrawn anytime for any reason.

Set your kids up to go as far as their dreams take them. With an RESP, contributions are matched by the government and grow tax-free.

Invest without any ceiling. No contribution limits, no withdrawal rules, no deadlines.

Access additional buying power and trade beyond your balance on margin, giving you the flexibility to act on opportunity.