Understanding capital gains and losses

Published: Oct 17, 2022

Updated: Apr 02, 2026

Learn what capital gains and losses are, how they’re calculated, and how they can affect your taxes.

Every time you sell an asset in an investing account, you generate either a capital gain or loss. While these gains and losses are pretty straightforward at their core, it can be helpful to understand what they are, how they’re calculated, and how they apply to your bottom line.

What are capital gains?

A capital gain is how much money you make on any asset you sell, whether it’s a stock, a bond, an ETF, an option, or even other assets like real estate. The Canadian government is very clear on how capital gains are calculated (opens in a new tab):

Adjusted Cost Base (ACB) means the cost of acquiring the asset, including the price you pay, commissions, legal fees, etc, and settlement costs mean the cost of selling that asset. For example, for calculating capital gains on a home or other real estate, your ACB on the purchase would include things like closing fees and legal expenses, and your settlement costs would include things like listing fees and real estate commissions.

For investments, the ACB is usually the price paid for a security plus any associated fees or commissions, and Settlement costs are usually any potential commissions or transaction fees on the sale. For example, if you bought a share of an example company (let’s call them EX) at $200, then later sold that share at $300, then your ACB and settlement costs would add up to $200 (plus commissions), and your capital gains would be about $100:

Please note: Since Questrade offers $0 commissions on stocks and ETFs, you may only see settlement costs in certain cases, such as when buying options, precious metals, or mutual funds, or when calculating ACB for shares transferred in from another brokerage.

How ACB works when buying at different prices

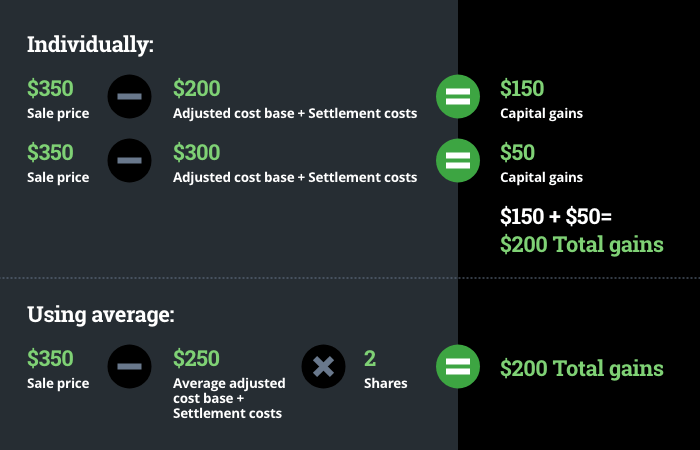

What would happen if, instead of selling in the example above, you bought another share at $300, and then later sold one of your shares at $350?

In this instance, the ACB would be averaged among your holdings. From a capital gains perspective, the extra EX share you buy at $300 is pooled into your current holdings of EX, averaging out the ACB:

So, even though the price went up by $150 since you bought your first share, the overall ACB is $250 per share, and your capital gain on the share you sold is $100.

What happens to the difference between profit-since-purchase and capital gain?

Since it’s using a rolling average, your ACB will balance out your overall gains in the long run, even if the costs are different on each transaction. So, if you immediately sold the second share at $350 as well, then it would also be considered to be sold at a capital gain of $100, even though the price only went up by $50 since you purchased that second share. Either way, your gains would add up to $200:

It’s worth noting that, when calculating tax purposes, ACB for multiple transactions of the same security is always represented as an average.

Important to remember:

Gains on open positions are known as “unrealized gains”, and will not count as capital gains until you close the position (usually by selling). Using the example above, if you bought two shares in a taxable account and later sold one, you would need to determine any capital gain or loss for tax purposes on the share you sold, but not for the share you’re still holding.

This ability to choose when to realize your gains can be helpful in tax strategies for taxable accounts. If you would like to learn how, please talk to a tax advisor.

What are capital losses?

When you understand capital gains, capital losses are pretty straightforward: they’re essentially just sales where you didn’t make your money back.

Using the reverse of the example above, if you bought an EX share at $300 and sold it at $200, you would calculate this as…

…or as a capital loss of $100.

Capital losses are never ideal, but they can be useful in tax strategies: capital losses can be used to offset and reduce any capital gains realized in the year. This means that closing a position at a loss in a taxable account could offset some of your taxable income in a strategy known as “tax-loss harvesting”.

Tax-loss harvesting in a taxable account can be a profitable strategy under certain circumstances, provided you know what you’re doing. If you would like to learn more about tax-loss harvesting, see our detailed tax-loss harvesting article or consult with a tax professional.

Please note that superficial losses (opens in a new tab) do not count as capital losses for tax purposes.

Capital gains, capital losses, and taxable income

While it can always be helpful to keep an eye on your gains and losses for your own information, capital gains and losses are only helpful from a tax perspective when they’re realized in a taxable account.

Tax-exempt accounts like your TFSA, FHSA, and RESP enjoy tax-free growth, meaning you don’t have to pay capital gains taxes (and therefore can’t claim capital losses).

Tax-deferred accounts like your RRSP grant tax deductions on contributions, and its holdings are only taxed when they are withdrawn from the account. In other words, any taxes on capital gains are deferred until you withdraw them.

Capital gains in taxable accounts, such as Cash accounts and Margin accounts, add to your taxable income.

If you’d like to know how your capital gains and losses impact your taxes, we strongly recommend consulting a tax expert. Or, if you’d like to learn more about tax-free growth, you may want to follow the links above to learn more about Canadian tax-advantaged accounts.

Ready to get started?

Download Edge Desktop on your PC or Mac now. Don’t have a Questrade account yet? Open one today to get started in minutes.