Note: The information in this blog is for information purposes only and should not be used or construed as financial, investment, or tax advice by any individual. Information obtained from third parties is believed to be reliable, but no representations or warranty, expressed or implied is made by Questrade, Inc., its affiliates or any other person to its accuracy.

Lesson TFSA 101

Can you retire off your Tax-Free Savings Account?

Understand how you can use your TFSA to save for retirement.

- What a TFSA is, and how it can help you save for retirement

- Why some people choose their TFSA as a retirement savings vehicle

- Whether the TFSA limits are high enough to be your sole retirement savings vehicle

It has been a while since we last looked at the question of whether you can retire off your Tax-Free Savings account (TFSA). Since then, Canadians over 18 have accumulated even more contribution room - $6,000 more as of this January. Based on this new contribution room, we’ve updated our numbers to see if you can retire off your TFSA – and how long you’ll need to save.

While the government of Canada does provide support for retirees in the form of both the Canada Pension Plan (CPP) and the Old Age Security pension (OAS), it is becoming increasingly evident to Canadians that achieving the retirement lifestyle you want will require a larger amount of money to be saved by individuals. And that’s why some people are turning to a TFSA.

Since it was first introduced in 2009, the Tax-Free Savings account has received a lot of attention in the media. Some people see TFSAs as a short-term investment account, but others are drawn to it for long-term goals – especially as a tool for retirement savings. Prior to this, a Registered Retirement Savings Plan (RRSP) was the only tax-advantaged way to save for your retirement, but now the younger TFSA seems to be gaining in popularity.

The TFSA works very differently than an RRSP. Contributions to an RRSP are tax-deductible and the funds grow tax free. However, withdrawals from your RRSP are considered income, so you have to pay income tax accordingly.

By comparison, you don’t get a tax deduction for money you contribute to your TFSA, but eligible investments are allowed to grow tax free. Also, when you want to make a withdrawal, your funds won’t be considered income. This difference has drawn the interest of some investors who want to lower their tax bills in retirement. In addition to providing a source of after-tax income during your retirement, TFSA withdrawals will not impact your eligibility for government benefits like OAS.

This is why some Canadians are becoming excited about using their TFSA to fund their retirement. However, there is an important question…

Is your TFSA enough to retire on?

It’s easy to see why some people might like the TFSA, but is it enough to retire off of? Let’s do the math.

For the purposes of this hypothetical situation, let’s assume that you are earning a monthly OAS amount of $635.26 per month ($7,623.12 per year) and a monthly CPP amount of $619.68 per month ($7,436.16 per year). Let’s also assume that in retirement, you spend the Canadian average of $2,667 per month, and to keep the math simple for this example we’ll ignore inflation.

The life expectancy in Canada continues to slowly climb, with the average life expectancy currently in the 80s. If you retire at age 65, and enjoy 20 years of retirement you’ll spend $640,080 over your retirement. Over those 20 years, you will earn $301,185.60 from your Canada Pension Plan and Old Age Security Benefits. This leaves you with a difference of $338,894.40 that you need to make up from your savings. Can your TFSA cover that gap?

Looking under the hood at your TFSA

At first glance, the answer is no. But the story doesn't end there.

The contribution room in your TFSA is increasing every year, with the TFSA contribution limit increasing by $6,000 this year. And remember, investments made in your TFSA account are tax-sheltered, meaning that you pay no income tax on eligible investment returns your TFSA earns – you could pay fees though, so you should monitor those and ensure you keep them under control.

Some of us have healthy TFSA accounts already, but for many of us that isn’t the reality. Many Canadians haven’t even opened a TFSA or maxed out their available contribution room. So let’s look at the opposite end of that and examine the situation for someone who doesn’t yet have a TFSA.

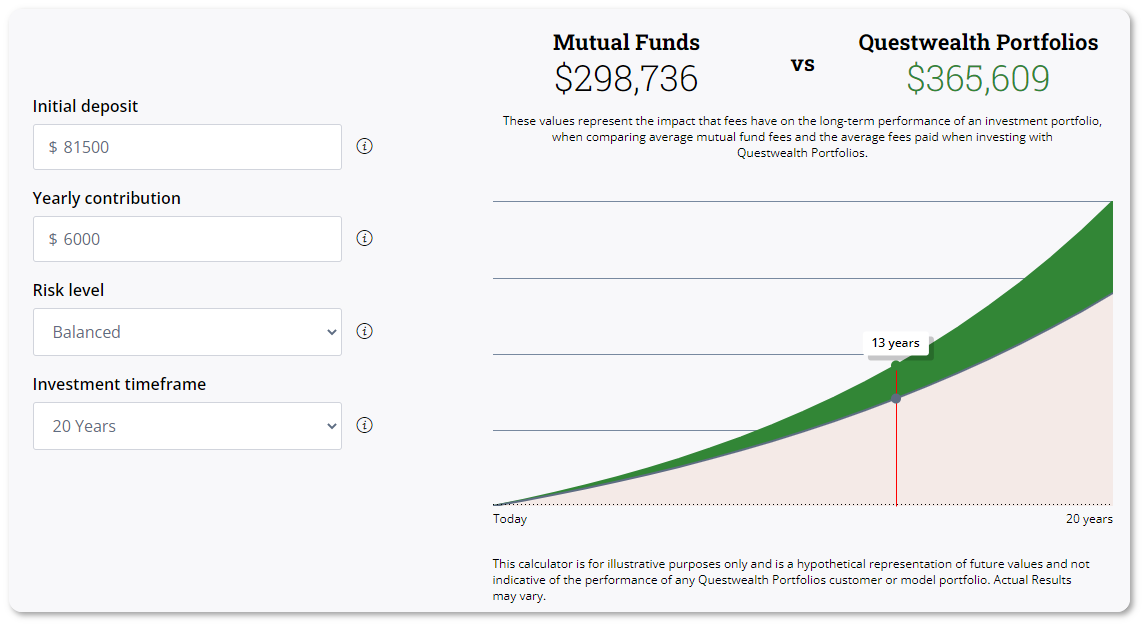

Let’s assume that you opened your first TFSA this year and maxed it out with a $81,500 contribution. If the TFSA contribution room continues to grow at $6,000 per year, and you invest your portfolio at a balanced risk level, how long will it be until you reach the magic number of $338,894.40?

According to our calculator it could take as little as 10 years (assuming an aggressive risk portfolio) – but it could take longer if you invest in higher fee investments. The excess fees that you might pay in one year mean that you have less money earning working to earn an investment return for you in subsequent years. In the long run, this can lead to a substantial difference in the potential size of your retirement portfolio.

What this means for you

Can you retire solely off your TFSA? Based on our examples, the answer depends on four things:

- Investment return

- How long you have to save money

- How much you'll spend in retirement

- How much you're paying in fees (lower fees can help you retire wealthier)

If you’re just starting to save for your retirement, you invest at a balanced risk level, and you plan on spending what the average Canadian does today in retirement…you might have a few years to go before you can retire the way that you want, but it definitely could be possible. If you keep the fees you pay under control, you could potentially manage to do it before your TFSA celebrates its thirteenth birthday.

By making use of the tax-advantaged savings opportunities that the government of Canada provides, while also keeping your investment fees under control, you build a stronger foundation for the secure and successful retirement of your dreams.

If you enjoyed this post, please consider sharing it on Facebook or Twitter!

Start investing confidently

Ready to open an account and take charge of your financial future? It's easy. Get started in minutes.

Related lessons

Want to dive deeper?

Accounts 101

Explore the different account types available in Questrade and determine the right account for you.

View lessonExplore

Margin 101

Learn about using a non-registered account and important information when leveraging it for your investments.

View lesson